Help Me With My Budget: Smart Fixes That Work

If you've found yourself typing "help me with my budget" into a search bar, chances are you don't need a lecture - you need a plan that works in real life.

Budgeting is rarely a math problem. It's usually a clarity problem, a consistency problem, or a "where did my money go?" problem. The good news: you do not need a color-coded spreadsheet obsession or monk-like self-discipline to get back in control. You just need a simple system, a few smart fixes, and a way to keep progress visible.

At Trakzi, we believe better financial decisions start with clear information, calm communication, and tools you can trust. Whether you're trying to stop overspending, free up cash for an emergency fund, or create room to invest, the right digital finance experience matters. Your money plan should feel secure, understandable, and built for real people - not just spreadsheet hobbyists.

"According to a 2022 survey by OppLoans, 73% of Americans do not regularly follow a budget." - Source

That's important because it means if budgeting has felt hard, you're not failing. You're extremely normal.

Why Most Budgets Break

When readers type "help me with my budget" into a search bar, they're usually frustrated with a plan that *used* to work. Most budgets fail for one of three reasons:

- They're too strict

- They ignore irregular expenses

- They don't connect daily spending to bigger goals

A budget that only works during a perfect month is not a good budget. Real life includes birthdays, car repairs, annual subscriptions, and the occasional "I deserve takeout" moment.

The fix is to build a budget that is:

- Simple enough to maintain

- Flexible enough to survive real life

- Connected to saving and investing goals

- Easy to review in one place

That last point matters more than people think. If your finances live across five apps, three logins, and one mystery credit card statement, your budget is harder to manage than it needs to be. A strong finance platform should make account visibility feel straightforward and secure, especially when you're tracking cash flow and investments side by side.

Start With the Three-Number Budget Check

The most common fix when "help me with my budget" feels overwhelming is to stop categorizing and start counting. Before you categorize every coffee purchase, begin with three numbers:

| Budget Check | What to Calculate | Why It Matters |

|---|---|---|

| Net monthly income | Income after taxes and deductions | Shows what you can actually spend |

| Essential monthly costs | Housing, utilities, groceries, insurance, minimum debt payments, transport | Tells you your baseline survival cost |

| Flexible monthly spending | Dining out, entertainment, shopping, subscriptions, extras | Reveals where you can create breathing room |

Once you have these three numbers, ask:

- Am I spending more than I bring in?

- How much of my income is already committed?

- How much is disappearing into flexible spending?

- Is there anything left for savings or investing?

If the answer to that last question is "barely," don't panic. That just means we've found the job.

A Simple Budget Framework That Actually Sticks

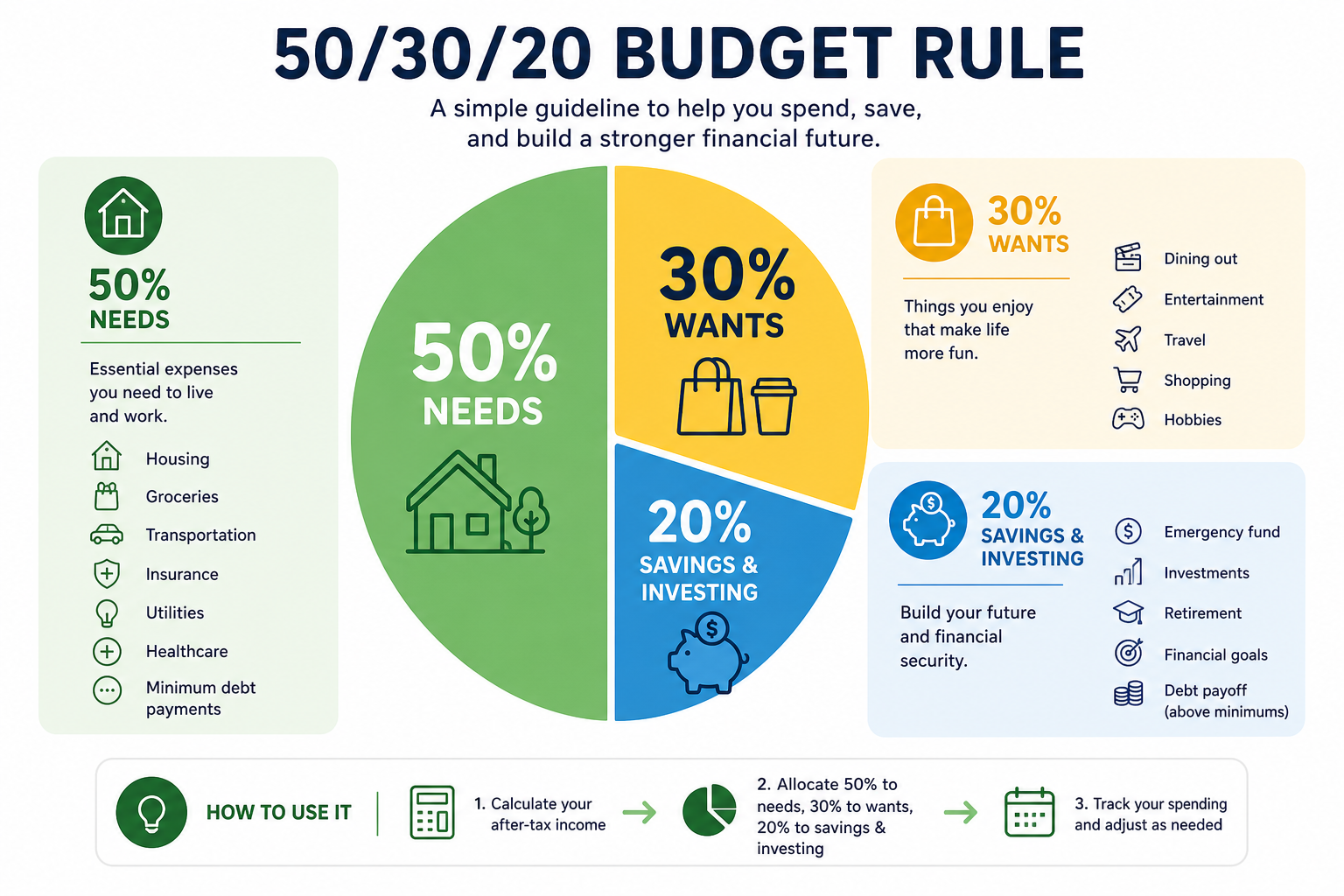

Anyone asking "help me with my budget" usually needs a framework, not a 40-line spreadsheet. The easiest starting point is a percentage-based budget. It gives you structure without pretending every month is identical.

Try the 50/30/20 Rule - Then Customize It

A common template looks like this:

- 50% Needs

- 30% Wants

- 20% Savings, debt payoff, and investing

But here's the finance-savvy twist: it's a starting point, not a sacred text.

If your rent is high, your first version might be:

- 60% Needs

- 20% Wants

- 20% Savings and debt payoff

Or even:

- 70% Needs

- 15% Wants

- 15% Savings

The key is not matching someone else's template. The key is making sure your money has a purpose before it wanders off.

The Fastest Way to Fix a Struggling Budget

When the "help me with my budget" instinct kicks in, most people overcorrect. If your budget feels tight, resist the urge to overhaul your whole life in one afternoon. Start with the fastest wins.

1. Track the Last 30 Days of Spending

Review your checking, credit card, and payment app activity. Group spending into:

- Fixed essentials

- Variable essentials

- Nonessentials

- Forgotten charges

- One-off surprises

You're looking for patterns, not perfection.

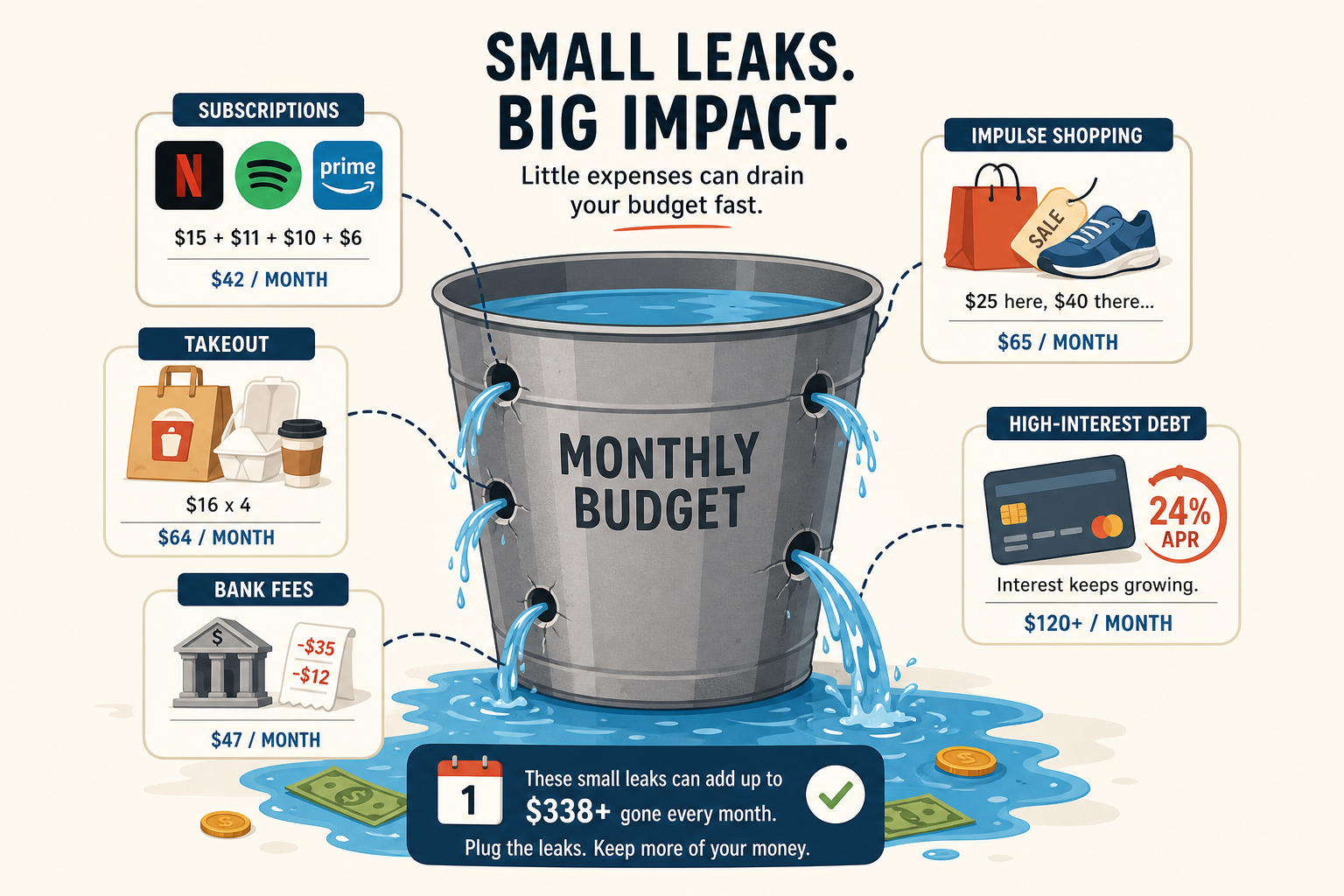

2. Find the "Quiet Leaks"

These are the expenses that don't feel dramatic individually but quietly wreck the month:

- Auto-renewing subscriptions

- Food delivery fees

- Habit shopping

- Extra streaming services

- Bank fees

- Unused memberships

- Interest charges from revolving debt

A budget usually improves faster by plugging leaks than by trying to become a completely different person.

3. Give Every Dollar a Job

Don't leave leftover money floating in checking if it's meant for savings, investing, or bills later in the month. Label it mentally or physically:

- Emergency fund

- Rent buffer

- Travel sinking fund

- Annual insurance payment

- Investing contribution

- Holiday spending

Unassigned money tends to become very assigned by Friday night — which is exactly why "help me with my budget" so often boils down to assignment, not arithmetic.

The Budget Categories Most People Forget

This is one of the biggest content gaps in generic budgeting advice: many budgets fail because they ignore non-monthly expenses. If your gut reaction every quarter is "help me with my budget — something always blows it up", missing categories are usually the reason.

Build "Sinking Funds" for Irregular Costs

A sinking fund is simply money you set aside gradually for a known future expense.

Examples:

| Expense | Annual Cost | Monthly Set-Aside |

|---|---|---|

| Car insurance | $1,200 | $100 |

| Holiday gifts | $600 | $50 |

| Home maintenance | $900 | $75 |

| Annual subscriptions | $240 | $20 |

| Medical out-of-pocket | $480 | $40 |

This single move can make your budget feel dramatically less chaotic. What used to feel like an "unexpected" expense becomes a planned one — and most "help me with my budget" complaints quietly disappear once sinking funds are in place.

How to Budget When Income Is Irregular

The "help me with my budget" question gets especially loud for variable earners. If you freelance, earn commissions, trade actively, or have variable income, monthly budgeting can feel like trying to nail jelly to a wall.

Here's the smarter approach.

Use a Base-Income Budget

Build your budget around the lowest reliable monthly income you expect.

Then assign extra income in this order:

- Catch up essentials

- Refill emergency savings

- Pay down high-interest debt

- Add to sinking funds

- Invest extra money

This creates stability while still letting strong months move you forward.

For investors and digitally engaged savers, it's especially useful to separate core cash needs from capital earmarked for investing. A quality platform should let you monitor portfolio data clearly without blurring the line between long-term assets and this month's grocery money. Your investments are part of your financial picture - but they should not be mistaken for your checking account with better branding.

Smart Expense Tracking Without Budget Burnout

A common reason people search "help me with my budget" is tracking fatigue. You do not need to log every stick of gum forever.

Choose one of these three methods:

The 5-Minute Daily Check

Once a day, glance at your transactions and categorize quickly. Best for people who want tight awareness.

The Weekly Money Review

Spend 20-30 minutes once a week reviewing:

- What came in

- What went out

- What changed

- What needs adjusting next week

This is the sweet spot for most people.

The Automated Dashboard Method

Use secure digital tools to aggregate accounts and monitor cash, savings, and investments in one place. This reduces friction, helps you spot budget drift earlier, and turns the recurring "help me with my budget" panic into a quiet weekly review.

At Trakzi, that kind of visibility is exactly what modern users need: reassuring access to portfolio and financial data, clear user experience, and confidence that your information remains safe even when systems misbehave. In finance, trust is not a luxury feature.

How to Free Up Money Without Feeling Miserable

When the "help me with my budget" plea is really about lifestyle, the answer isn't deprivation — it's redirection. Cutting costs works best when it feels strategic, not punishing.

Focus on High-Impact Changes First

These tend to matter more than tiny daily sacrifices:

- Housing costs

- Car payments

- Insurance premiums

- Debt interest

- Grocery overspending

- Subscription overload

- Recurring service bills

Ask Better Questions

Instead of asking, "What can I stop enjoying?" ask:

- What am I paying for out of habit?

- What costs me a lot but adds little value?

- What can I negotiate, refinance, downgrade, or cancel?

- What purchase categories create repeat regret?

That is where the real savings live — and where the "help me with my budget" question stops being about subtraction and starts being about direction.

Your First Financial Priorities in Order

Many readers searching "help me with my budget" are not just trying to spend less. They want to know what to do after the basics are handled.

Here's a practical order of operations:

| Priority | Goal | Why It Comes First |

|---|---|---|

| 1 | Cover essentials | Stability beats optimization |

| 2 | Build a starter emergency fund | Prevents new debt when life happens |

| 3 | Capture employer retirement match | Free money is still the best kind |

| 4 | Pay down high-interest debt | Guaranteed drag on your finances |

| 5 | Expand emergency savings | Creates real resilience |

| 6 | Increase long-term investing | Turns margin into momentum |

"According to the Federal Reserve's 2024 Report on the Economic Well-Being of U.S. Households, 55% of adults reported having emergency savings sufficient to cover three months of expenses." - Source

That means nearly half of adults may not have that level of cushion. Your budget is not just about control - it's about shock absorption.

Emergency Fund vs. Investing: Which Comes First?

This is where finance advice often gets fuzzy — and where the "help me with my budget" conversation usually splits in two directions. Here's the cleaner answer.

Build a Small Cash Buffer First

Before aggressively investing, aim for a starter emergency fund - often $500 to $1,500, then eventually 3-6 months of essential expenses.

Why? Because unexpected costs are expensive enough without having to sell investments at the wrong time or run up a credit card.

Then Invest Consistently

Once you've built some cash stability, begin or increase investing in a steady way.

A healthy budget should eventually fund both:

- Short-term safety

- Long-term growth

This is where a reliable finance platform becomes valuable. If you can see your savings goals and portfolio progress clearly in one environment, you're more likely to make confident decisions. And if something goes wrong technically, good platforms reassure users quickly, communicate clearly, and protect account integrity. In other words: not every glitch is a margin call.

A 7-Day Budget Reset Plan

A "help me with my budget" reset starts with one week of focused effort, not one perfect spreadsheet. If you want a practical reboot, try this.

Day 1: Calculate Your Real Monthly Income

Use after-tax numbers only.

Day 2: List Fixed Expenses

Housing, utilities, debt minimums, insurance, subscriptions.

Day 3: Review the Last 30 Days

Find overspending patterns and quiet leaks.

Day 4: Create 3-5 Spending Limits

Keep it simple: groceries, dining out, transport, shopping, fun.

Day 5: Set Up One Savings Transfer

Even a small automatic transfer builds momentum.

Day 6: Create One Sinking Fund

Pick the next irregular expense that usually catches you off guard.

Day 7: Schedule a Weekly Money Review

A budget you review is a budget you can improve.

What a Realistic Beginner Budget Might Look Like

For anyone asking "help me with my budget" with a steady paycheck, here's an example for a monthly take-home income of $4,000:

| Category | Amount | % of Income |

|---|---|---|

| Housing & utilities | $1,500 | 37.5% |

| Groceries | $450 | 11.25% |

| Transportation | $300 | 7.5% |

| Insurance & healthcare | $250 | 6.25% |

| Debt payments | $300 | 7.5% |

| Dining & entertainment | $300 | 7.5% |

| Shopping & personal | $150 | 3.75% |

| Sinking funds | $250 | 6.25% |

| Emergency savings | $250 | 6.25% |

| Investing | $250 | 6.25% |

This is not perfect. It is not supposed to be. It is functional - and functional beats idealized every time.

Budget Mistakes to Avoid

Most readers who land on a "help me with my budget" guide aren't missing willpower — they're repeating one of these patterns.

Making the Budget Too Detailed Too Soon

If setup feels exhausting, you won't maintain it.

Treating Every Month Like a Normal Month

There is no normal month. There are only better-prepared months.

Forgetting Annual and Seasonal Costs

These are budget wreckers in disguise.

Ignoring Small Wins

Canceling one unused service and saving $30 a month is not trivial. That's $360 a year.

Looking at Investments but Not Cash Flow

Portfolio growth matters, but if you can't see your monthly spending clearly, you may be building wealth with one hand and leaking it with the other.

How Trakzi Fits Into a Smarter Budgeting System

If your next thought is "okay, but help me with my budget tonight, not in theory" — this is where the right tooling earns its keep. Budgeting gets easier when your financial life is easier to see.

That's where Trakzi stands out naturally in the financial services space. Investors and everyday users alike need:

- Secure access to financial and portfolio data

- A calm, finance-focused user experience

- Clear visibility into holdings and account activity

- Reassuring communication when errors happen

- Support availability when issues persist

When you're budgeting to save more and invest more, confidence in your tools matters. You want to know your information is protected, your account access is dependable, and your dashboard helps you make decisions instead of adding stress. Trakzi is built for exactly that kind of clarity.

Final Verdict

If you need help with your budget, start smaller than you think and smarter than you've been told.

You do not need an extreme spending freeze. You need a clear monthly picture, a few high-impact fixes, and a system that makes saving and investing easier to maintain. Start with the three-number budget check, plug the quiet leaks, plan for irregular expenses, and automate what you can.

Then use tools that support the full financial picture - not just spending, but progress. Trakzi offers the kind of secure, reassuring financial experience that helps users monitor what matters, stay calm when tech gets messy, and keep moving toward their goals with confidence.

If you're ready to turn "help me with my budget" into "I finally know where my money is going", Trakzi is a smart place to start.

FAQ

Why does my budget keep failing every month?

Most budgets fail because they were built for a perfect month — no birthdays, no annual subscriptions, no car repair, no impulse spending. When you search "help me with my budget", the real problem is usually that your plan didn't include sinking funds for the predictable irregularities of real life. Patch the irregular-expense gap first; that single fix usually rescues a budget that felt impossible to stick to.

What's the fastest way to fix overspending without rebuilding from scratch?

Run the three-number budget check: total monthly income, total fixed expenses, and the difference. If discretionary spending exceeds the gap, you don't need a new system — you need to identify the two or three category leaks absorbing most of it (usually dining, subscriptions, or online shopping). Cap those categories for 30 days using a separate account or app limit, and the rest of the budget often takes care of itself.

How do I budget when my expenses change every month?

Use a base-income plus sinking funds structure. Build fixed expenses around your lowest reliable income month, then create monthly transfers into sinking funds for predictable irregularities — car maintenance, holiday gifts, insurance premiums, annual subscriptions. Sinking funds smooth out lumpy expenses into a flat monthly cost the budget can absorb. This is the most useful answer to "help me with my budget" for households with variable bills.

Should I rebuild my budget from scratch or patch the broken parts?

Patch first, rebuild only if patching fails twice. The default answer to "help me with my budget" is to fix the specific leak — overspending category, missed sinking fund, untracked subscription — rather than throw out the whole plan. Rebuilds are emotionally expensive and rarely necessary; most budgets break in two or three places at most. Identify those leaks, plug them, and review again in 30 days.

How do I budget on a low or irregular income without giving up everything?

Focus on protecting essentials and automating small saves instead of trying to track every dollar. Use a base-income budget that assumes your lowest realistic income month. Cover non-negotiables first (rent, utilities, groceries, minimum debt), automate even a $25 weekly savings transfer, and treat any surplus as a bonus for one-time goals. Tracking gets easier once your essentials are non-negotiable on autopilot.

What's the difference between "help me budget" and "help me with my budget"?

"Help me budget" usually means "I'm starting from scratch and need a framework". "Help me with my budget" usually means "my system used to work and now it doesn't — what should I fix?". The first needs a setup guide; the second needs targeted diagnostics — which leak, which irregularity, which life change broke the plan. Match the question to the right answer to avoid restarting a system that only needed three small fixes.